During the populist revolt of 2016, which first led to the “shocking outcomes” of Brexit and then Trump, we cautioned that these phenomena were merely the “silent majority” of the developed world’s middle class expressing their anger and frustration with a world that has left them – and their real disposable income – behind, while rewarding the top 1% through policies that have led to a relentless and record ascent in global asset prices, largely the purview of the world’s wealthiest.

More recently, we also noted that it was only a matter of time before this latest “revolt” fizzled, as the realization that changing one politician with another would achieve nothing, and anger shifted to the real catalyst behind growing global inequality (and anger): central banks.

In his latest note today, Albert Edwards picks up on this theme to write “Theft redux: the citizens will soon turn their rage towards Central Bankers.” The core of his argument is familiar:

While politics in the West reels from a decade of economic crisis and stagnation, asset prices continue to surge on the back of continued rapid growth in G3 QE. In an age of “radical uncertainty” how long will it be before angry citizens tire of blaming an impotent political system for their ills and turn on the main culprits for their poverty – unelected and virtually unaccountable central bankers? I expect central bank independence will be (and should be) the next casualty of the current political turmoil.

That’s just the beginning from Edwards, who appears to be getting increasingly angrier and more frustrated with a market that makes increasingly less sense: his fiery sermon continue with the following preview of the “inevitable catastrophe that lies ahead.”

Evidence of the impact of monetary madness on assets prices is all around if we care to look. I read that a parking spot in Hong Kong was just sold for record HK$5.18 million ($664,200). What about the 3.5x oversubscribed 100 year Argentine government bond? Sure, everything has a market clearing price, even one of the most regular defaulters in history.

But what concerned me most about the story was it was demand from investors (“reverse enquires”) that prompted the issue. Is it just me or can I hear echoes of the mechanics of the CDO crisis? But no one cares when the party is still raging and investors, drunk with the liquor of loose money, are blind to the inevitable catastrophe that lies ahead.

There is a lot of anger out on the streets, as demonstrated most visibly in recent elections. Even in France where investors feel comforted that a “moderate” has gained (absolute?) power, it is salutary to remember that the two establishment parties have just been decimated by a man who had never before stood for public office!

This is perhaps even more radical than Trump’s anti-establishment victory under the Republican umbrella. The global political situation is incredibly fluid and unpredictable. While a furious electorate has turned its pent up anger on the establishment political parties, the target for their rage is misguided. I am not completely alone in thinking it is the unelected and virtually unaccountable central bankers who are primarily responsible for the poverty of working people and who will be ultimately held to account in the next crisis.

In the immediate aftermath of the 2008 financial crisis, politicians skilfully diverted the publics’ anger away from themselves by scapegoating “the bankers”. After another eight years of economic stagnation that excuse no longer is tenable and politicians themselves are now taking the flak. But citizen revolutionaries will, I think, soon turn their fire on those who I believe are truly responsible for their plight.

We explained back in January 2010 in a note entitled Theft! Were the US & UK central banks complicit in robbing the middle classes? how central banks in the US and UK had deliberately stocked up massive housing bubbles prior to the Global Financial Crisis (GFC) to disguise the rapid rise in income inequality in both countries. Rapidly rising house prices allowed the middle classes to maintain the illusion they were getting richer so that despite stagnant real incomes they could continue to consume by extracting housing equity. We know how that party ended!

After the GFC central bankers have collectively spent the last decade stepping up the pace of money printing to new extremes in an attempt to drown the global economy in liquidity, while couching their actions in plausible theories such as “secular stagnation”.

There is no recognition at all by central bankers that it may well be their own easy money and zero interest rate policies that are actually causing the stagnation in growth while at the same time wealth inequality surges to intolerable heights. Yellen et al will inevitably be sacrificed at the altar of political expediency as citizen rage explodes.

Edwards continues, justifying why it has taken his 2010 prediction so long to play out, and predicting that the end result is nothing short of a full systemic break down:

My dire prognostications back in January 2010 proved premature. It has taken another seven years of economic stagnation and falling living standards of working people, together with the sight of the rich getting richer as a result of central bank QE polices, for the patience of ordinary working people to snap – most visibly in the US and UK elections. That rage has not diminished and, as Bill Gross predicted, the system is in the process of breaking down.

Amidst the current turmoil in the US and UK there is a huge sigh of establishment relief in the eurozone in the wake of the defeat of the far right in recent French and Dutch elections.

The establishment hope the tide towards radicalism has turned – at least in continental Europe. That belief is wrong in my view and the current revolution will devour more political and establishment victims before it’s over, most notably the central bankers themselves.

Ultimately, it’s all about wealth inequality however, and here it is central bankers again who are at fault:

Anecdotally we all know wealth inequality has risen due to central bank QE and free money. Although we can see and feel it, it is reassuring to see firm evidence. This week the UK Resolution Foundation published a damning report into rising wealth inequality in the UK (this UK think tank is led by David Willetts, who during his political career was known as one of the most intellectual of MPs – his nickname being “two brains”). The report found the key driver for rising inequality was the collapse in UK home ownership since the 2008 financial crisis to a 30 year low: link and link.

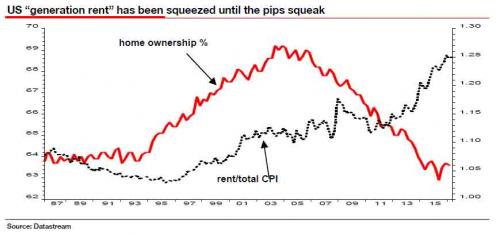

Like so many economic commentators and think tanks, the Resolution Foundation doesn’t seem to want to pin the proverbial tail on the donkey – for it is not the lower homeownership that is the real problem per se but the fact that QE is driving up asset prices that households no longer own! (In addition, zero interest rates have driven up buyto- let investment demand for housing hence reducing the supply of housing for owner occupation). While UK home ownership is now at a 30-year low (link), the US too has seen a similar shocking plunge in home ownership (see chart below).

At least in the run-up to the 2008 GFC, owner occupation in the UK and US surged along with house prices and so working people had the illusion they were getting richer along with the rest of the population. Now there is no such illusion for what has been dubbed “generation rent”. In the US, to add insult to injury, rent inflation has rapidly outstripped CPI since the GFC.

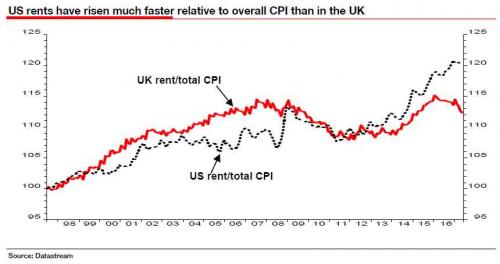

If things are bad in the UK, ?generation rent? has been squeezed far more badly by soaring rents in the US (see chart below). No wonder the JAMs (just about managing) are in revolt.

There is much more, bust the gist is clear: it is only a matter of time before the general population realizes that it is not politics, but monetary policy. But how long? The simple answer: as long as stocks keep rising, all shalle be well: “no one cares when the party is still raging and investors, drunk with the liquor of loose money, are blind to the inevitable catastrophe that lies ahead.”

Which is also why the Fed will do everything in its power to keep the market ascent – and its existence – continue for as long as possible. And then, as a last diversion, they will blame Trump.

In other words, by the time all of this happens, the angry natives may have no choice but to rent their pitchforks…