Institutionalizing the speculative excesses that inflated the previous housing bubble has fed magical thinking and fostered illusions of phantom wealth and security.

The global housing market has been dominated by magical thinking for the past 15 years. The magical thinking can be boiled down to this:

A person who buys a house for $50,000 will be able to sell the same house for $150,000 a few years later without adding any real-world value. The buyer will be able to sell the house for $300,000 a few years later without adding any real-world value. The buyer will be able to sell the house for $600,000 a few years later without adding any real-world value.

And so on, decade after decade and generation after generation: a house should magically accumulate enormous capital (home equity) without the owner having to do anything but pay the mortgage for a few years.

- Former Reagan Treasury Secretary James Baker: Supports Reinstating Glass-Steagall To Stop Rothschild Banking Cabal!

- Decommission Banks For Credit Unions: Reinstall The Glass Steagall Act To Protect American Citizens From The 1% Sociopaths.

- How Free Americans Became Slaves To The Rothschild Bankers: Glass Steagall Act Will Stop Them ~ You Know, The One Billy Clinton Repealed In 1999 That Allowed The Housing Bubble!

- Repeal Now The True Damage To The United States: The Surreptitious $12.8 Trillion TARP Bailout.

- Breaking => U.S. Citizens Stuck With Billions In Obama Orchestrated TARP Losses: States Must Nullify The Printed Paper Bailout ~ TARP Ceiling Was Raised 117 Times From $787 Billion To A Hidden $12.8 Trillion!

- Obama’s $12.8 Trillion Banker’s Gambling Debt Bailout: Black Unemployment ~ 16.7% Highest In 27 Years, But Lower Than Overall Unemployment ~ Overall Real Unemployment is 23% Of Which 79.96% Are White!

The capital isn’t created by magic, of course: it’s created by a greater fool paying a fortune for the house on the speculative confidence that an even greater fool will magically appear to pay an even greater fortune for the same house a few years hence.

This is the result of housing transmogrifying from shelter purchased to slowly build equity over a lifetime of labor into a speculative bet that credit bubbles will never pop. This transmogrification is the final stage of the larger dynamic of financialization, which turns every asset into a speculative commodity that can leveraged via debt and derivatives and sold into global markets.

The magic of something for nothing is especially compelling to a populace whose earnings have stagnated for decades. The housing bubble fed the fantasy that a household could set aside next to nothing for retirement and then cash out their “winnings” in the housing casino when they reached retirement age.

What believers in the sustainability of the housing casino conveniently ignore is the enormous risk (and debt) being taken on by the last greater fool: if the buyer pays cash, they are gambling on rents continuing to skyrocket along with home valuations, though these two are not as correlated as many assume.

Younger buyers have less disposable income than their elders due to deteriorating wages, higher student loan debt and higher taxes on earned income. As a result, the risk of their defaulting or being impoverished by the collapse of housing valuations is much higher than the risks faced by the buyers who rode the first bubble up to (ephemeral/phantom) riches.

The only way a young household can buy a $150,000 house for $600,000 is if interest rates are low enough to enable a modest income to leverage a huge mortgage. This is the basis of the Federal Reserve’s campaign to buy Treasury bonds and mortgages: by driving interest rates to unprecedented lows, the Fed enables marginal buyers to become the last greater fool.

The first housing bubble circa 2001-2008 inflated as a result of financialization. The second, current echo-bubble has inflated on the socialization of financialization: the FHA and other government agencies have essentially taken over the entire mortgage market, guaranteeing or backing 95% of all mortgages, while the Fed has pushed rates down to historic lows to enable marginal buyers to make bets in the housing casino.

Robert Rubin (70th Secretary of the Treasury under Bill Clinton) & A Member Of Rothschild’s Covert Council On Foreign Relations

The Elites Responsible For Orchestrating The Destruction Of The Glass Steagall Act Of 1933 Are As Follows:

Goldman Sachs:

Alan Greenspan

Rothschild Federal Reserve:

Alan Greenspan

Larry Summers

Citibank:

Sandy Weill

John Reed

Robert Rubin

Traveller’s Insurance:

– Volubrjotr

The current echo-bubble has another speculative source: cash buyers of homes to rent. About a third of all home sales in many markets are cash buyers, speculators hoping to cash in on the bubble by selling to a greater fool, or investors seeking the safe returns of rental housing.

Unbeknownst to the majority of these investors, there is no guaranteed return in rental housing when you overpay for the property and a recession guts demand for rentals. This is another form of magical thinking: nothing ever goes down.

The stock market goes higher forever, housing goes higher forever, and the Fed has banished recessions forever. If this isn’t magical thinking, then what is it? Faith in the New Normal? Based on what?

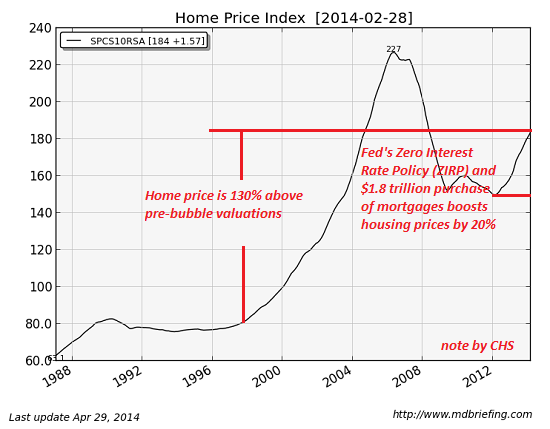

Let’s quantify the magical thinking and the echo bubble with a few charts. Home prices are still 130% above pre-bubble valuations.

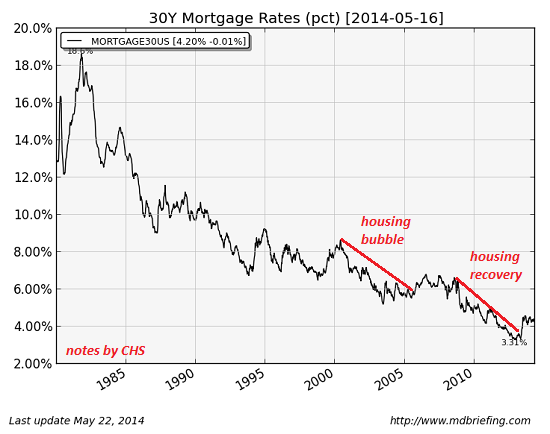

Declining mortgage rates (courtesy of the Fed) fueled the first housing bubble and the current echo-bubble.

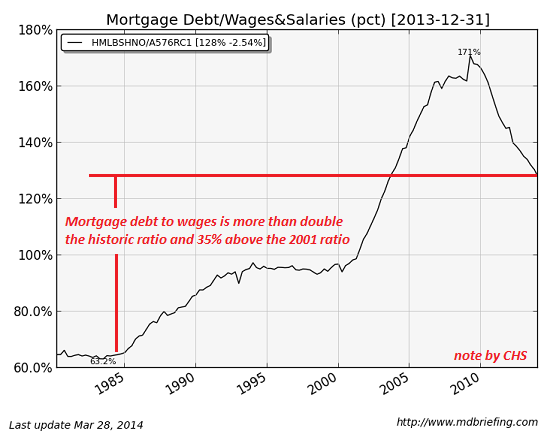

Measured by houshold earned income, mortgage debt is more than double the historic average of wages-to-mortgage-debt.

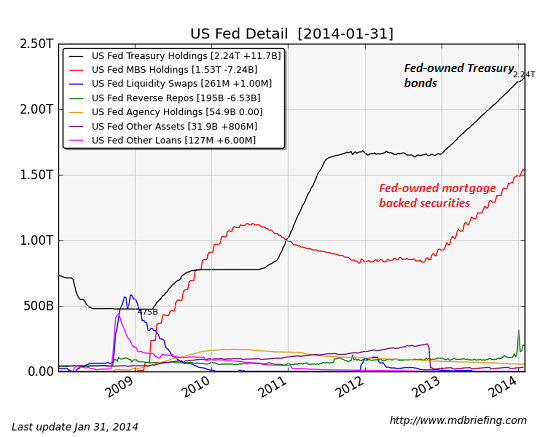

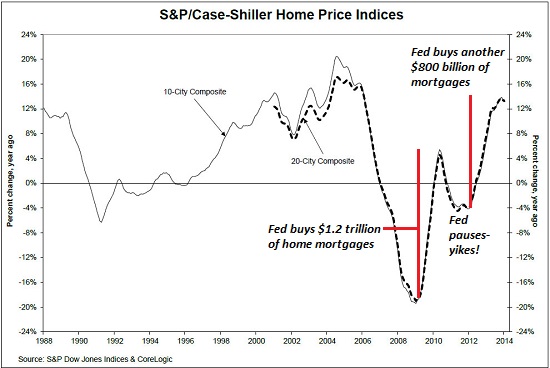

Take a look at the Fed’s purchases of mortgages: from zero to $1.2 trillion, and then another $800 billion for good measure. The Fed has intervened in the Treasury market to the tune of almost $2 trillion to suppress interest rates.

The Fed’s pause in mortgage purchases caused the housing market “recovery” to nosedive. This should make us wonder what will happen when the Fed’s mortgage purchases finally end.

Relying on greater fools and expecting the rental housing market to magically ignore the ravages of recession for the first time in history is not a formula for financial or speculative success. The current echo-bubble in housing will pop, just like every other leverage/credit-fueled speculative bubble in history.

Institutionalizing the speculative excesses that inflated the previous housing bubble has fed magical thinking and fostered illusions of phantom wealth and security. The damage that will be unleashed by the echo-bubble deflating will be substantial, and in line with the The Smith Uncertainty Principle, not as predictable as many imagine:

The Smith Uncertainty Principle: Every sustained action has more than one consequence. Some consequences will appear positive for a time before revealing their destructive nature. Some consequences will be intended, some will not. Some will be foreseeable, some will not. Some will be controllable, some will not. Those that are unforeseen and uncontrollable will trigger waves of other unforeseen and uncontrollable consequences.

Max Keiser

Related Articles:

- 7 Rip-Offs Of The New World Order Are As Old As The Hills.

- Dead Bankers & You: The Coup Against The United States Of America!

- Obama’s Coup d’etat Of America: What If The Citizens Of The United States Knew The Truth?

- Thank You Mr Obama For Reminding Us Why We Should Be Ever Vigilant: In Fact 252 Reasons Why!

- China & Russia Have Been Dumping U.S. Dollars Since 2010: Takes Several Years For Impact ~ Its Now 2014.

- Two Soviet Senators Chucky Schumer & Al Franken Told IRS To Target Constitutionalists! Rothschild’s Sovietism Ended In Russia On 25 December 1991.