The EU Sows the [same] Seeds [for] of the Greek Economic Crisis:

In sowing the seeds of the Greek crisis, European politicians have made the same mistakes as American politicians before the financial and banking crisis of 2008-09, that is to say encourage excessive indebtedness of some economically weak countries with loan guarantees.

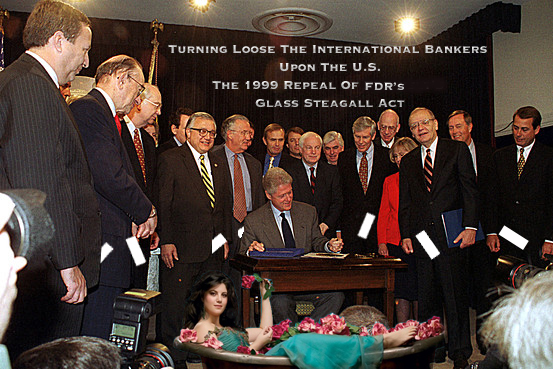

What really created the conditions for a major financial and banking crisis in the U.S., starting in 1999 when the so-called Glass-Steagall Act of 1933 was abolished by the administration of Bill Clinton, was the innovation of insurance given to risky loans.

![President Roosevelt [FDR] Signing the Glass-Steagall Act July 16, 1933. Preventing Banks From Meddling With The U.S> Economy. Separating Investment From Commercial Banking.](https://politicalvelcraft.org/wp-content/uploads/2015/07/2010-03-05-glasssteagle.jpg)

In the U.S., the regulatory agencies that are the U.S. Treasury (controlled by mega banks) and the central bank (the Fed) (controlled by mega banks) closed their eyes when risky banking products were created, not the least being the famous derivative products such as the mortgage-backed CDOs (collateralized debt obligations) whose risk of default was artificially reduced with insurance contracts (the famous Credit Default Swaps or CDS) against payment default and issued by large insurance companies such as AIG (American International Group).

In doing so, borrowing was greatly encouraged and bank lending became more risky. It resulted in a mountain of mortgage debt, which led to the creation of a speculative housing bubble that began collapsing in 2005, and which turned into a general global financial crisis in 2008-09.

However, European politicians seem to have made the same mistake as American politicians. In their case, they encouraged a rise in the public debt of the poorest countries in the Eurozone by giving guarantees against default to large banks if they continued lending to them despite growing risks.

This is what enabled a government like the Greece government, for example, to continue piling on debt upon debt even though lenders would have by themselves stopped lending, if they had not received guarantees against default.

Today, the Greek debt represents an unsustainable 177 percent of its annual GDP (yearly total domestic production). Indeed, when a country’s debt exceeds 100 percent of its gross domestic product (GDP), creditors begin to get nervous. They react normally by raising interest rates and by reducing the volume of their loans.

But in Europe, politicians wished to keep interest rates as low as possible on loans to the most economically weak countries of the Eurozone. In doing so, they created, in 2010, the European Financial Stability Facility (EFSF), with guarantees from member States, in proportion to their participation in the European Central Bank (ECB).

At a minimum, the EFSF has secured 131 billion Euros of Greek debt. Thus German taxpayers, for example, are on the hook for 41.3 billion Euros of guaranteed Greek debt, while French taxpayers, through their government, are responsible for 31 billion Euros of that debt, and so on for the other 17 member countries of the Eurozone. In so doing, an economic debt problem has been transformed into a major political issue.

Now, European politicians who gave a public guarantee to a large part of the Greek debt fear the political consequences if they were to pass the buck of the Greek government’s default on its debt to their own taxpayers.

On the other hand, large banks and other lenders, confident in the guarantees they obtained from other European governments, feel no inclination to ‘restructure’ down the Greek government’s debt. In other words, everything is frozen.

In a normal situation, creditors would bear alone the risks undertaken in lending to a government already deeply in debt, and they would have to write off some of the bad debt on the books.

This is reminiscent of the American situation before the 2008-09 financial crisis when mortgage lenders would not accept to reduce the mortgage debts of borrowers because their claims had been [surreptitiously] secured against default by insurance contracts to that effect. We know how it was resolved.

American taxpayers were called to the rescue of mega banks and mega insurance companies, either directly through the U.S. Treasury or indirectly through the central bank (Fed), the latter acquiring from the banks toxic assets at full price. The same scenario is likely to occur in the Eurozone, whether Greece remains or not in the monetary union. In that sense, last Sunday’s Greek referendum on July 5 did not change anything.

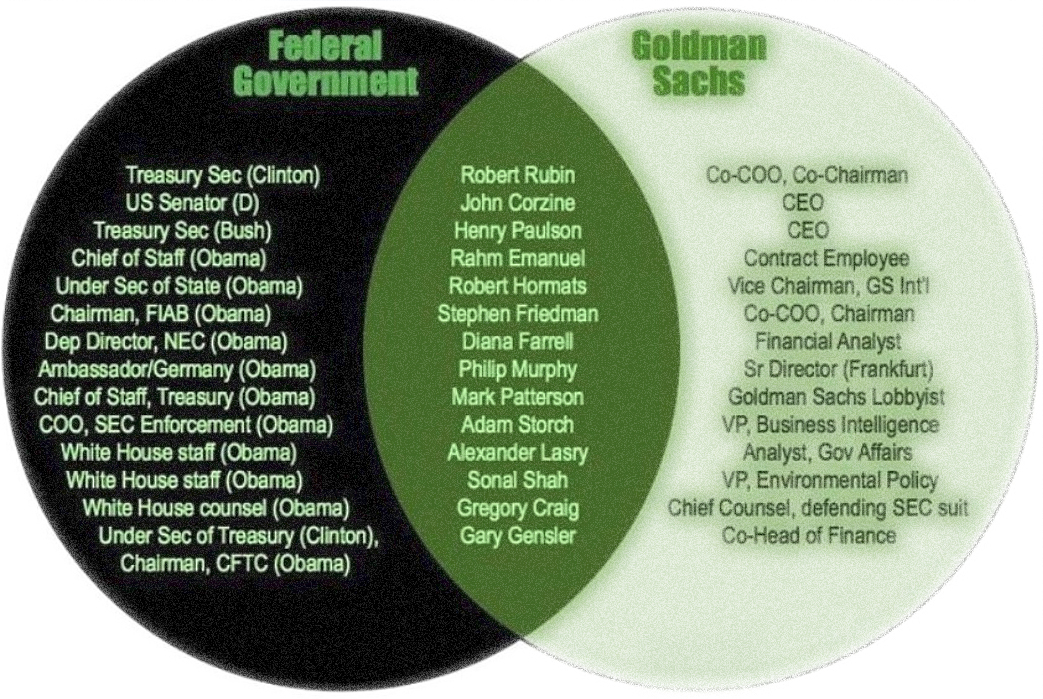

In the Greek case, it has to be remembered that international investment banks, especially Goldman Sachs, used derivatives and dubious accounting tricks to camouflage the extent of the Greek government‘s debt in order to meet the strict requirements to join the Eurozone and allow Greece to join the monetary union.

The main criteria to join the Eurozone are a public deficit below 3% of GDP and a public debt level lower than 60 % of GDP.

It is on these last two criteria that Goldman Sachs assisted the Greek government, in 2001, in presenting a rosy and false financial picture of its real deficit and its real debt level. Why European banking authorities allowed themselves to be lured by these tricks is another matter that should one day be clarified.

Rodrigue Tremblay, Montreal, July 6, 2015

Another Banker Suicide Added To The List Of 72 Dead By Un-Natural Causes!

Silver is being slammed below $15 right now [July 7, 2015] and everyone that was waiting for the Bad Guy’s final slam…this is it!

Why now? Here’s a short list:

1) Today is the COMEX reporting cutoff day for the last trades of the 2nd Quarter. The 3rd Quarter 2015 is their planned global market meltdown to hit in the last month of the quarter…September.

2) [J.P. Morgan] JPM is now rumored to have CLOSED OUT their huge paper short and dumped it on Citibank.

3) JPM is MASSIVELY long physical silver according to Ted Butler.

4) The European Derivative Complex is breaking down due to Greek derivatives.

5) The September/October collapse is close at hand.

Everything points to this being the LAST SILVER SLAM EVER!!!

~ Bix Weir

Related Articles:

- Greece and the Euro: Towards Financial Implosion

- Greece Will Adopt the Bitcoin If Eurogroup Doesn’t Give Us a Deal

- Bitcoin Now Doing $200 – $300 Million Dollars Of Transactions Per Day!

- The People vs The Banks ~ Without Firing A Shot: Catholic Subsidiarity!

- Hillary Clinton Pledges to Defend Israeli Apartheid and Fight BDS Movement

- Bitcoin hits four-month high as Greece votes ‘no’ to eurozone bailout conditions

- Bill Clinton’s “Rothschild-Inspired Decisions” Triggered Three Major Crises In Our Times!

- When Saving Interest Rates Go Negative: Time For New Medium Of Exchange Bitcoin & Quark!

- Remember 1 Year Ago -> US Banks Told To Be Prepared For 30-day Crisis ~ Rothschild’s Last Stand!

- More Proof Of The Banker’s Nefarious NWO: The Confidential Memo At The Heart Of The Global Mafia Financial Crisis.

- Bill Clinton Father Of 2014 Financial Fallout: Clinton’s 1999 Deregulation Of Rothschild Wall Street ~ Documents Reveal “Push To Pilfer” America’s Wealth!

- Dark Legislation ~ Dodd Frank & Basel III Enacted Treason Against The United States July 2, 2013: Wealth Funneled Into Rothschild’s [BOE] Bank Of England.