The Consumer Financial Protection Bureau (CFPB) has set up an online database of financial horror stories that shows what happens when an average American interacts with one of the financial supermarkets (a/k/a universal banks) that grew out of the repeal of the investor protection legislation known as the Glass-Steagall Act. The complaints are concentrated against the biggest Wall Street banks.

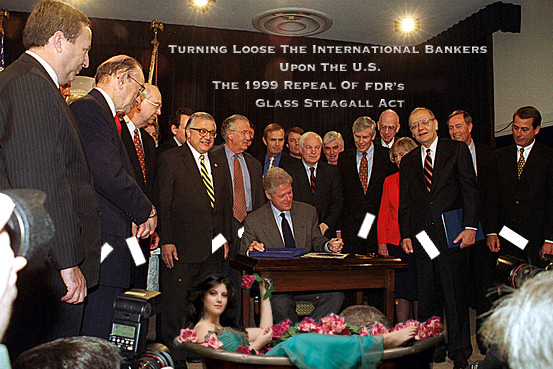

- Billy Clinton Turned Loose The International Banks Upon The U.S. 1999

- Father Of The U.S. Financial Debacle: Bill Clinton Allowed The Banks To Manipulate The Markets Beginning In 1999

If you are one of the lucky Americans who has not already been mugged in the shopping aisles of the financial supermarkets, you should carefully browse through the database to see what awaits the unwary. Just go to the complaint archive, and place the name of any bank you want to examine in the upper right-hand search box.

- Searching under the name Citibank (part of the Wall Street behemoth Citigroup) will bring up 29,000 rows of complaints.

- A search under Chase, part of the mega Wall Street bank, JPMorgan Chase, brings up 37,000 rows of complaints.

- After years of being charged by Federal regulators for abusing their customers and the public trust, both U.S. banks became felons on May 20 of last year when they admitted to felony charges related to rigging foreign currency markets.

Wall Street banks are intended to function as efficient allocators of capital to grow new businesses and industries in America. But since the Glass-Steagall Act was repealed in 1999 under pressure from Citigroup, Wall Street’s biggest banks increasingly function as legalized loan sharking operations – targeting the poor, minorities and financially unsophisticated.

In what has become a highly efficient, wealth transfer mechanism, billions of dollars each month move from the pockets of those least able to protect themselves from financial abuse to the coffers of the one percent in America who sit in the executive offices of these banks.

![President Roosevelt [FDR] Signing the Glass-Steagall Act July 16, 1933. Preventing Banks From Meddling With The U.S> Economy. Separating Investment From Commercial Banking.](https://politicalvelcraft.org/wp-content/uploads/2015/07/2010-03-05-glasssteagle.jpg?w=578&h=486)

That protection was removed when President Bill Clinton signed into law the Gramm-Leach-Bliley Act on November 12, 1999, the legislation that repealed the Glass-Steagall Act. After protecting the nation for 66 years, it took just 9 years after its repeal for Wall Street to implode, taking the U.S. economy with it.

Bill Clinton and his Treasury Secretary, Robert Rubin, ushered in the era of the financial supermarket that has trapped America in a time warp of 1920s-style abuses on Wall Street and the income and wealth inequality that it has spawned.

Rubin had the audacity to head straight for Citigroup’s Board after stepping down as U.S. Treasury Secretary, collecting $126 million in compensation over the next decade.

This year Senator Bernie Sanders’ supporters were able to pressure the Democrats to include the restoration of the Glass-Steagall Act into this year’s Democratic Party Platform, but political watchers were shocked that it also ended up in the Republican Party’s Platform as well.

- Bernie Sanders Embraces Oligarchy

- Lying Piece Of Shit Bernie Sanders Embraces Oligarchy –> Sells Out The United States & Blocks Transparency On Federal Reserve!

The financial atrocities coming out of the publicly accessible database set up by the CFPB has sent a chill through both parties. Behind the scenes, both Democrats and Republicans believe there could be another epic crash like that of 2008 and neither wants the other party pointing the finger and saying, you blocked us from restoring the Glass-Steagall Act.

- Barney Frank – The True Tea Bagger!

- Barney Frank Is Preventing Glass Steagall From Being Legislated: Glass Steagall Will Nullify Fraudulent Derivative Debt Bailout

[Usury:]

Consider Complaint Number 2073454 at the CFPB database which was received on August 20, 2016. The individual states that Citibank has increased the interest rate on his or her credit card to 29.99 percent for paying “a few days late.” The individual also states that “I have been a long time customer of Citi.”

This high interest rate is not an aberration. Citigroup provides credit and services the credit cards for major retailers like Home Depot, Macy’s, Bloomingdale’s, Brooks Brothers and others. Many of the cards are issued under the name Department Stores National Bank, a subsidiary of Citigroup. The Macy’s card agreement currently shows an interest rate of 25.49 percent as does the Bloomingdale’s card. The Home Depot credit card from Citibank says its annual percentage rate varies from 17.99 to 26.99 “based on your creditworthiness.”

But consider what Citibank is paying struggling Americans who have their savings and Certificates of Deposit (CDs) with its insured bank. Savings accounts with Citi earn from one-tenth of one percent interest for accounts below $10,000 to eight-tenths of one percent for accounts of $500,000 or more. Five year CDs at Citibank are one-half of one percent. That’s less than half the yield of a 5-year U.S. Treasury note, which yields 1.19 percent.

Now consider how generous the U.S. government was with taxpayers’ money when Citigroup imploded as a result of its own corrupt devices in 2008.

- The government infused $45 billion in equity into Citigroup and provided more than $300 billion in asset guarantees.

- Secretly, the Federal Reserve gave Citigroup more than $2 trillion cumulatively in revolving low-interest loans, billions of dollars of which were below 1 percent interest.

- Citigroup was insolvent, a bad risk and there was no guarantee the taxpayer would ever be paid back.

- Did the government charge this subprime risk 29.99 percent interest? No, it gave the bank a rate compatible with a triple-A rated company that was providing impeccable collateral.

- Closing In On The IRS Thief: IRS paid at least $6 billion in child tax credits to people who weren’t eligible!

- General Electric Makes New Lear Jet In Mexico Where Unemployment is 4.9%: U.S. Taxpayers Bailed Out G.E. For $182.5 Billion. Thanx G.E.

- Obama Cuts Welfare, While His Economic Advisory Board Chairman Increases American Poverty: Jeff Immelt, CEO Of General Electric & Owner Of NBC Urges More Welfare Debt For America ~ While Receiving $Billions In Taxpayer Bailout Money From Obama & Then Moves American Jobs Out To Other Countries, While Obama Nullifies Tax Oblgations For G.E.

In an interview with Bill Moyers on March 16, 2012, John Reed, who created Citigroup with co-CEO Sandy Weill by merging together Citibank with the investment bank, Salomon Brothers, the brokerage firm, Smith Barney, and Travelers Group, an insurance company, explained the real motivation behind the deal – which had been sold to Congress as keeping American banks competitive with European rivals:

MERGING CONGLOMERATES INTO FASCIST DICTATORS!

John Reed: “Sandy Weill. I mean, his whole life was to accumulate money. And he said, ‘John, we could be so rich.’ Being rich never crossed my mind as an objective value. I almost was embarrassed that somebody would say out loud. It might be happening but you wouldn’t want to say it.

“But you know, the biggest bonus I had ever received when I was at Citi was three million dollars. The first year I worked with Sandy it was 15 [$15 million]. I said to the board, ‘I’m the same guy doing the same job, same company. There are two of us. The company’s bigger but there’re two of us. What’s going on?’ ‘Oh, you don’t understand.’ And it was just totally different culture. And see, Wall Street developed that culture.”

Weill retired from Citigroup after reaping more than $1 billion in total compensation while Reed stepped down after receiving an estimated $300 million in compensation plus an annual pension of more than $2 million.

The thousands of complaints against Citibank in the CFPB archive, many dated as recently as this year and last, are only a slight variation of the same customer abuses we have been reading about since Citigroup’s financial supermarket was formed in 1998 – in violation at the time of the Glass-Steagall Act.

On July 20, 2001, Gail Kubiniec, a former Assistant Manager of a Citigroup subsidiary, CitiFinancial, testified as follows to the Federal Trade Commission (FTC):

“At CitiFinancial, emphasis was placed on marketing new loans, particularly real estate loans (loans secured by a home mortgage), to present borrowers of CitiFinancial. Employees would receive quarterly incentives, called ‘Rocopoly Money,’ based on how many present borrowers they ‘renewed’ (refinanced) into new loans…

Typically, employees would only state the total monthly payment amount in selling a proposed loan. Additional information, such as the interest rate, and the financed points and fees, closing costs, and ‘add-ons’ like credit insurance, were only disclosed when demanded by the borrower…It was also common practice to try to sell borrowers the largest loan possible…

All CitiFinancial branch offices had quotas for the sale of credit insurance…Loans were typically presented to consumers with ‘100% coverage,’ meaning that real estate loans were presented with at least credit life and disability already included, and personal loans were presented with at least credit life, disability, involuntary unemployment, and property insurance already included…

The pressure to sell coverages came from CitiFinancial’s Regional and District Managers.”

The FTC also had testimony from Michele V. Handzel, a former Branch Manager for CitiFinancial:

“CitiFinancial put much more pressure on employees than the Associates did [a firm merged into CitiFinancial] to include as many credit insurance and ancillary products as possible on every loan….

In fact, I feel that the credit insurance sales practices at CitiFinancial were worse than at The Associates. From January to June 2001, the policy was that no personal loan at CitiFinancial would be approved if it did not include some type of credit insurance, nor would a real estate loan be approved without some type of ancillary product…

There were several internal measures in place to effectuate this policy. For instance, District Managers would frequently refuse to send a loan to underwriting if it did not include some type of insurance product. Moreover, loans that were closed and did not include any insurance would be identified by CitiFinancial’s internal insurance auditors, and the employee who closed the loan would be written up…

Closings at CitiFinancial resembled those at The Associates – they were brief. Personal loan closings took approximately 10 minutes. Real estate loan closings took a little longer but also did not provide a lot of details about the loan. At CitiFinancial, I was instructed to do a ‘closed folder’ closing, meaning that information would be discussed orally first. Only after the borrower indicated that he wanted to sign would the employee open the folder and have the borrower sign the papers.”

On August 28, 2001, an Ohio woman sent the following complaint to a Federal agency:

“This will be my 3rd request for someone from this dept to assist me. I am a victim of predatory lending. Citifinancial gave me a loan at 24.99% in June of ’99. I had a perfect credit score. The[y] called me back into their office one week later. Refinanced that same loan at 18.99% and had a check for $500.00 waiting for me…this time they told me that I had to use my home as collateral to get the lower interest rate…

I feel that because I am a female and black that they…thought they could get away with this…”

Did the FTC have evidence to show that CitiFinancial was targeting minorities and the vulnerable? According to their former Assistant Manager, Gail Kubiniec:

“I and other employees would often determine how much insurance could be sold to a borrower based on the borrower’s occupation, race, age, and education level. If someone appeared uneducated, inarticulate, was a minority, or was particularly old or young, I would try to include all the coverages CitiFinancial offered. The more gullible the consumer appeared, the more coverages I would try to include in the loan…”

The FTC settled their suit against CitiFinancial on September 19, 2002 for $215 million. The Consumer Financial Protection Bureau was created under the Dodd-Frank financial reform legislation of 2010. It has picked up where the FTC left off.

- Central Bankers & US Government Now Preparing For Dodd Frank Basel III Bail-Ins.

- Call Boy & Barney Frank Connection? : Homosexual Prostitution And Pedophile Criminal Acts!

- The ‘Man of Steel’ Is Just More Propaganda From A Protected Racket: By Ex Senator Christopher Dodd ~ Current Chairman Of The Motion Picture Association Of America!

On July 2015, the CFPB ordered Citibank to:

“provide an estimated $700 million in relief to eligible consumers harmed by illegal practices related to credit card add-on products and services. Roughly 7 million consumer accounts were affected by Citibank’s deceptive marketing, billing, and administration of debt protection and credit monitoring add-on products. A Citibank subsidiary also deceptively charged expedited payment fees to nearly 1.8 million consumer accounts during collection calls. Citibank and its subsidiaries will pay $35 million in civil money penalties to the CFPB.”

- Obama U.S. State Dept. Pedophilia Cover-Up.

- DOD Inspector General: Obama’s DOD Employees Charged Casino Transactions Totaling $3.4 Billion On Federal Credit Cards.

Illegal add-ons? Wasn’t that what Gail Kubiniec had told the FTC was happening back in 2001? The following complaint was received by the CFPB on May 22 of this year:

“A few months ago, I realized that Citibank had charged me [redacted] dollars each month for payment safeguard, a service I never signed up for, and that the CFPB has called an unfair and deceptive practice. I called and asked to quit the program and said I wanted a refund, and was given a fee adjustment of $700.00. Today I realized that even after that, I’ve still been incurring monthly payment safeguard charges…”

It is now enshrined in Federal court documents that Citigroup is a recidivist. U.S. District Judge Jed Rakoff used that very word to describe Citigroup in 2011 and 19 securities law professors told the Second Circuit Appellate Court the same thing in a related Amicus brief.

Since the chronology of serial charges against Citigroup (shown below) proves beyond a shadow of a doubt that Citigroup is not only an unreformed recidivist but a serial abuser of its own customers in its insured bank, its investment bank and its other subsidiaries, it is time for Congress to do its job and reinstate the Glass-Steagall Act and restore confidence and sanity to the U.S. financial system.

If there is any doubt that, as Bernie Sanders likes to say, fraud is now a business model on Wall Street, you can also check out JPMorgan Chase’s charges of wrongdoing here.

Chronology of Financial Abuses at Citigroup: (only a partial listing):

September 19, 2002: FTC Announcement — “In the largest consumer protection settlement in FTC history, Citigroup Inc. will pay $215 million to resolve Federal Trade Commission charges that Associates First Capital Corporation and Associates Corporation of North America (The Associates) engaged in systematic and widespread deceptive and abusive lending practices.”

October 31, 2003: U.S. District Court Judge William Pauley signs a settlement order agreed to by multiple regulators for Citigroup to pay $400 million over issuance of fraudulent stock research.

May 28, 2004: The Federal Reserve announces a $70-million penalty against Citigroup Inc. and CitiFinancial Credit Co. over their handling of high-interest-rate “subprime” mortgages and personal loans.

May 31, 2005: SEC announces a $208 million settlement with Citigroup over improper transactions by its proprietary mutual funds.

June 28, 2005: Citigroup agrees to pay the UK regulator, the FSA, $25 million over its “Dr. Evil” trade that manipulated the European bond market.

March 26, 2008: Citigroup settles a suit with Enron creditors for $1.66 billion over claims it aided and abetted Enron in hiding its debt.

August 26, 2008: California Attorney General Edmund Brown Jr. announces a settlement with Citigroup to return all monies improperly taken from customers through an illegal account sweeping program. According to the Attorney General:

“Nationally, the company took more than $14 million from its customers, including $1.6 million from California residents, through the use of a computer program that wrongfully swept positive account balances from credit-card customer accounts into Citibank’s general fund…The company knowingly stole from its customers, mostly poor people and the recently deceased, when it designed and implemented the sweeps,” Attorney General Brown said. “When a whistleblower uncovered the scam and brought it to his superiors, they buried the information and continued the illegal practice.”

December 11, 2008: SEC forces Citigroup and UBS to buy back $30 billion in auction rate securities that were improperly sold to investors through misleading information.

February 11, 2009: Citigroup agrees to settle lawsuit brought by WorldCom investors for $2.65 billion.

July 29, 2010: SEC settles with Citigroup for $75 million over its misleading statements to investors that it had reduced its exposure to subprime mortgages to $13 billion when in fact the exposure was over $50 billion.

October 19, 2011: SEC agrees to settle with Citigroup for $285 million over claims it misled investors in a $1 billion financial product. Citigroup had selected approximately half the assets and was betting they would decline in value.

February 9, 2012: Citigroup agrees to pay $2.2 billion as its portion of the nationwide settlement of bank foreclosure fraud.

August 29, 2012: Citigroup agrees to settle a class action lawsuit for $590 million over claims it withheld from shareholders knowledge that it had far greater exposure to subprime debt than it was reporting.

July 1, 2013: Citigroup agrees to pay Fannie Mae $968 million for selling it toxic mortgage loans.

September 25, 2013: Citigroup agrees to pay Freddie Mac $395 million to settle claims it sold it toxic mortgages.

December 4, 2013: Citigroup admits to participating in the Yen Libor financial derivatives cartel to the European Commission and accepts a fine of $95 million.

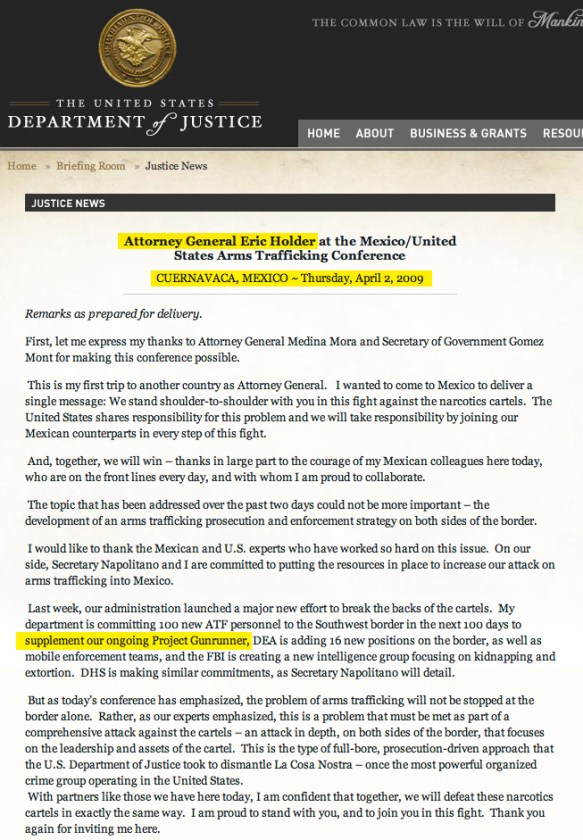

July 14, 2014: The U.S. Department of Justice announces a $7 billion settlement with Citigroup for selling toxic mortgages to investors. Attorney General Eric Holder called the bank’s conduct “egregious,” adding, “As a result of their assurances that toxic financial products were sound, Citigroup was able to expand its market share and increase profits.”

- ATF, DOJ Accomplice to Murder – Holder Had Knowledge Of Project Gunrunner In 2009

- Federal Judge Rules Congressional Lawsuit Against Obama’s DOJ Can Proceed: Eric Holder Is Already In Contempt Of Congress!

November 2014: Citigroup pays more than $1 billion to settle civil allegations with regulators that it manipulated foreign currency markets. Other global banks settled at the same time.

May 20, 2015: Citicorp, a unit of Citigroup becomes an admitted felon by pleading guilty to a felony charge in the matter of rigging foreign currency trading, paying a fine of $925 million to the Justice Department and $342 million to the Federal Reserve for a total of $1.267 billion.

February 23, 2016: The CFPB ordered Citibank to provide nearly $5 million in consumer relief and pay a $3 million penalty for selling credit card debt with inflated interest rates and for failing to forward consumer payments promptly to debt buyers. It took a second action against both Citibank and two debt collection law firms it used that falsified court documents filed in debt collection cases in New Jersey state courts. The CFPB ordered Citibank and the law firms to comply with a court order that Citibank refund $11 million to consumers and forgo collecting about $34 million from nearly 7,000 consumers.

Related Articles: